'Narendra Modi returning as PM but...' - Brokerage on Election verdict

June 05,2024

Emkay Global Financial Services anticipates Narendra Modi's return as Prime Minister in the upcoming elections, but warns that he will govern under significantly altered economic circumstances. Despite political continuity, the fundamental drivers of India's economic momentum are projected to remain steady, providing a stable backdrop for growth.

However, critical factor market reforms, including those related to land, agriculture, and labour, are no longer expected to advance. Privatization and asset monetization initiatives also face significant risks, potentially stalling.

Market Derating on the Horizon

Emkay Global foresees a market derating in the short term due to heightened risk perception. They believe the Nifty will present attractive valuations below the 20,000 mark, offering investment opportunities despite the immediate uncertainties.

Sectoral Shifts: PSUs and Capital Goods Vulnerable

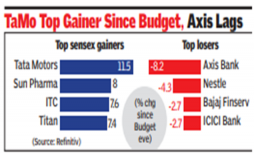

The report suggests a strategic shift from Public Sector Undertakings (PSUs) and capital goods to the Fast-Moving Consumer Goods (FMCG) sector. PSUs and capital goods are identified as the most vulnerable sectors amid the changing economic landscape.

Manufacturing and Capex Focus

Despite these challenges, the focus on manufacturing is expected to continue, given its critical role in job creation. The capital expenditure (capex) cycle may experience a slowdown as the government slightly pivots towards increased spending in other areas.

Emkay Global projects a comeback in consumption, with FMCG and value retailers poised for a strong return. This shift underscores a renewed focus on consumer-driven growth, adapting to the evolving economic environment.

In summary, Emkay Global foresees Narendra Modi's return as PM amidst significant economic changes. With key reforms stalled and privatization efforts facing hurdles, a short-term market derating is anticipated, making Nifty valuations below 20,000 attractive. Investors are advised to shift focus from PSUs and capital goods to FMCG and value retailers, while manufacturing and capex cycles may experience a slowdown.